Delta Dynamics: The Directional Compass of Options Trading

If you have ever traded options, you have likely encountered Delta. It is the most intuitive of the "Greeks," often referred to as the directional engine of your position. While Gamma measures acceleration, Delta tells you your current velocity relative to the underlying asset's price.

What is Delta?

Mathematically, Delta represents the first derivative of an option's value with respect to the change in the underlying asset's price.

In plain English: If the underlying stock moves up by $1, Delta tells you approximately how much your option's price will move in response.

The Delta Ranges

- Call Options: Have positive Delta (ranging from 0 to 1.0). As the stock goes up, the call value increases.

- Put Options: Have negative Delta (ranging from -1.0 to 0). As the stock goes up, the put value decreases.

The Three Faces of Delta

Delta is more than just a price sensitivity metric; professional traders use it in three distinct ways:

1. The Hedge Ratio

Delta tells you how many shares of the underlying asset you need to buy or sell to make your position "market neutral." For example, if you own 10 call contracts with a 0.50 Delta, your position behaves like owning 500 shares of stock. To hedge this perfectly, you would need to short 500 shares.

2. The Probability Proxy

While not mathematically perfect, a common "rule of thumb" among floor traders is that an option's Delta represents its percentage chance of expiring In-the-Money (ITM).

- A 0.15 Delta option has roughly a 15% chance of finishing profitable at expiration.

- An At-the-Money (ATM) option usually sits near 0.50 Delta, representing a coin-flip.

3. Directional Exposure

Delta quantifies your "directional bias." A high Delta means you are aggressively betting on a move, while a low Delta means you are looking for stability or betting on other factors like time decay (Theta) or volatility (Vega).

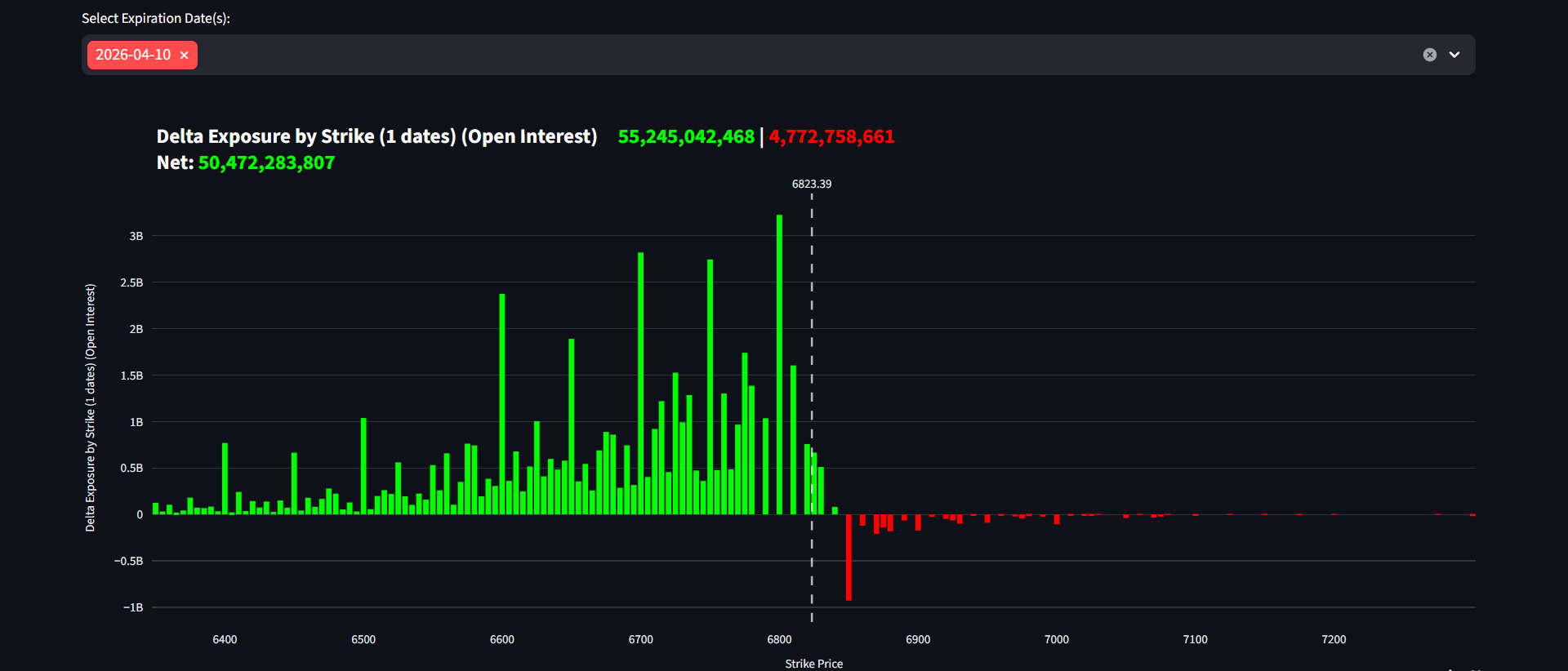

Analyzing SPX Delta Exposure

In the S&P 500 (SPX) markets, Delta analysis is critical for understanding market liquidity and potential "pinning" levels.

Analysis of Delta exposure across various SPX strikes.

Analysis of Delta exposure across various SPX strikes.

As seen in the chart above, Delta exposure tends to cluster around key psychological levels. Professional institutional desks monitor these "Delta walls" because they often act as support or resistance levels where market makers are forced to adjust their hedges.

Delta Sensitivity: The Role of Gamma

It is important to remember that Delta is not static. As the stock price moves or as time passes, Delta changes. This change is governed by Gamma (which we covered in our previous article).

"Delta is your position's direction; Gamma is how fast that direction changes."

Summary for Traders

- ITM Options: Have Deltas approaching 1.0 (or -1.0), meaning they move almost dollar-for-dollar with the stock.

- OTM Options: Have low Deltas, making them cheaper but highly speculative with a lower probability of success.

- Delta Neutrality: The goal of many institutional strategies is to keep total portfolio Delta near zero to profit solely from volatility or time.

Mastering Delta is the first step in moving from a casual speculator to a professional risk manager. It is your compass in the volatile seas of the derivatives market.