Charm: The Invisible Erosion of Directional Exposure

While Theta is the well-known Greek that measures the loss of an option's value over time, there is a more subtle "time-related" Greek that professional risk managers watch closely: Charm.

Also known as Delta Decay or Delta Bleed, Charm reveals the silent shifts in your directional exposure as the clock ticks forward.

What is Charm?

Mathematically, Charm is the second-order derivative of an option's value with respect to both price and time. More simply, it measures the rate at which an option's Delta changes as time elapses.

In plain English: Charm tells you how much your Delta will increase or decrease over a 24-hour period, assuming the underlying price and volatility remain constant.

Why Does Charm Matter?

Charm is the reason why a "Delta-neutral" position on Friday might no longer be neutral by Monday morning, even if the stock hasn't moved.

1. The Weekend Effect

Market makers and institutional desks are hypersensitive to Charm. As expiration approaches, the Delta of Out-of-the-Money (OTM) options "bleeds" toward zero, while the Delta of In-the-Money (ITM) options "pulls" toward 1.0. This natural drift requires constant re-hedging.

2. Market Magnetism

Large clusters of Charm can act as "magnets" or "repellers" for price action. As time passes, the changing hedge requirements of large institutions can create predictable flows in the market.

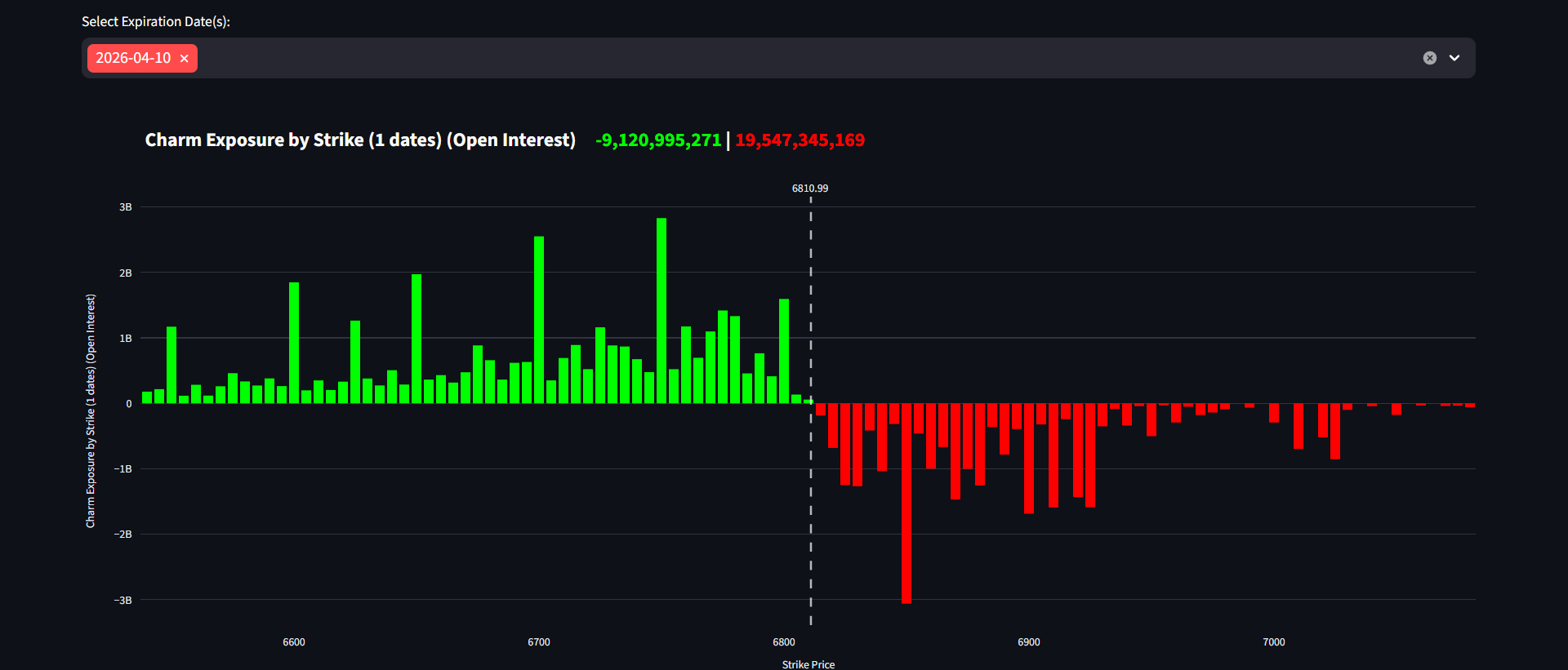

Analysis of Charm exposure and its impact on S&P 500 hedging levels.

Analysis of Charm exposure and its impact on S&P 500 hedging levels.

The chart above illustrates how Charm exposure shifts across different strike prices in the SPX. Understanding these levels allows a trader to predict where liquidity might dry up or spike as time runs out on a contract.

Charm in the Physics Context

Returning to our physics analogy:

- Delta: Velocity.

- Gamma: Acceleration.

- Vanna: Atmospheric Drag (Volatility).

- Charm: Is like Traction Loss or Frictional Erosion. Even if you are cruising at a constant speed (Delta), the slow wear and tear of time (Charm) slightly alters your path and efficiency over long distances.

Summary for Strategic Traders

- OTM Options: Charm causes Delta to decay toward zero as expiration approaches. Your directional bet becomes less sensitive to price moves.

- ITM Options: Charm causes Delta to pull toward 1.0 (or -1.0), meaning the option begins to behave exactly like the underlying stock.

- The "Silent Hedge": Managing Charm allows you to stay ahead of the "Monday Morning Gap" by anticipating how time will naturally shift your exposure.

In the world of derivatives, time is not just about losing value (Theta); it’s about the changing structure of your risk. Mastering Charm is the final step in truly understanding the "Ghost in the Machine" of the options market.