The Power of Gamma: Why It Rules the Options Market

In the world of options trading, the “Greeks” serve as the dashboard for managing risk. While Delta tells you how much your option’s price will move for every $1 change in the underlying asset, Gamma is the engine under the hood that dictates how fast that Delta changes.

What is Gamma?

Mathematically, Gamma is the second derivative of the option price with respect to the underlying asset’s price. More simply, it measures the rate of acceleration for Delta.

If Delta is the “speed” of your option price, Gamma is the “acceleration.” When an option has high Gamma, its Delta can jump from 0.20 to 0.80 very quickly, making the position significantly more sensitive to market moves.

Key Characteristics of Gamma

- At-the-Money (ATM) Peak: Gamma is highest when the underlying price is near the option’s strike price. This is where the uncertainty of whether the option will expire “in” or “out” of the money is greatest.

- Time Sensitivity: As expiration approaches, Gamma for ATM options increases dramatically. This “Gamma explosion” is why prices can swing wildly on expiration day (often referred to as “Pin Risk”).

- Long vs. Short:

- Long Gamma: When you buy options, you are “Long Gamma.” Your Delta becomes more positive as the price goes up and more negative as it goes down, which can accelerate profits.

- Short Gamma: When you sell options, you are “Short Gamma.” This is risky because the market can move against you at an accelerating rate, requiring constant adjustments.

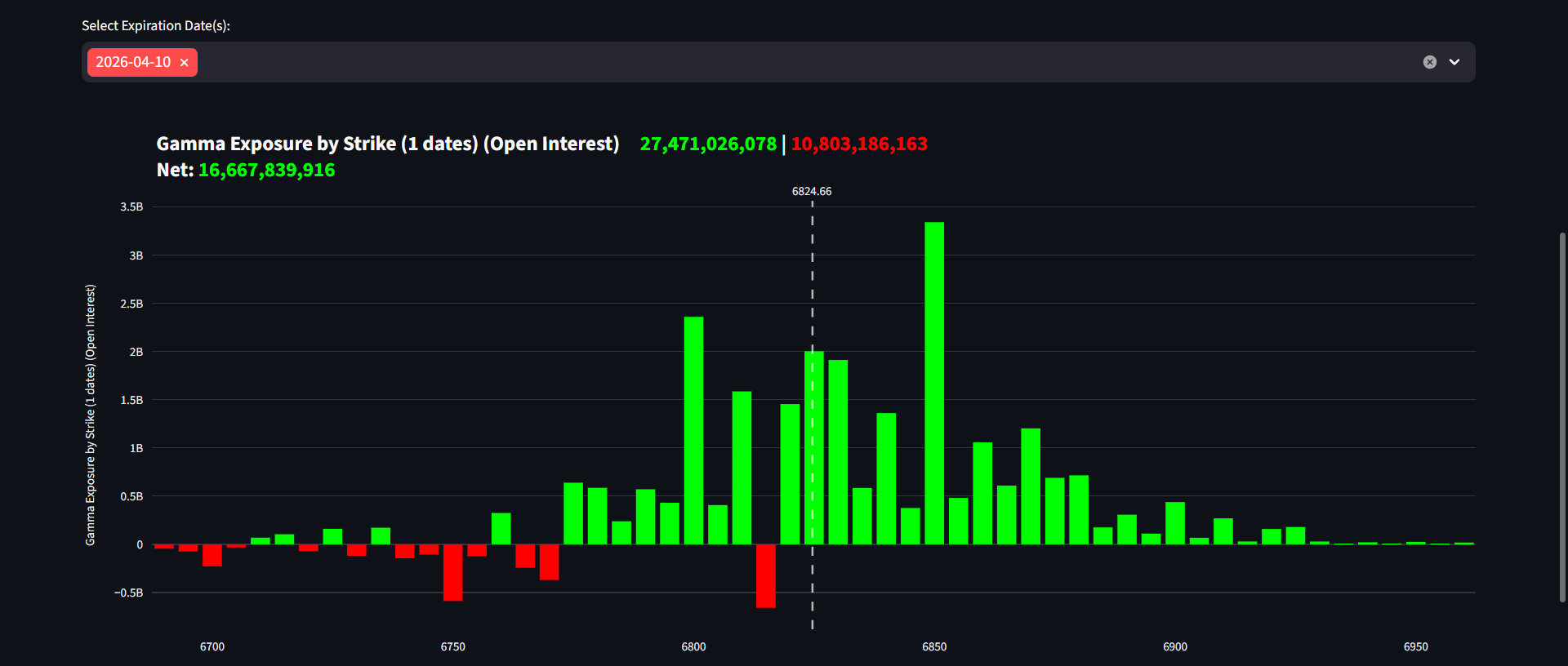

Typical Gamma exposure by strike visualization.

Typical Gamma exposure by strike visualization.

Why is Gamma a Critical Derivative?

Gamma is often considered the most important Greek for institutional traders and market makers for several reasons:

- Market Maker Hedging: Market makers must stay “Delta Neutral.” If they are short Gamma, they are forced to buy more of the underlying asset as it rises and sell as it falls to stay balanced. This “hedging” can create feedback loops that increase market volatility.

- Gamma Squeezes: When a massive amount of call options are bought, market makers must hedge by buying the stock. This drives the price up, which increases the Gamma, forcing them to buy even more stock. This phenomenon can lead to explosive price rallies.

- Risk Management: Understanding Gamma allows traders to predict how their exposure will change. It warns them when a position might become “unmanageable” due to extreme sensitivity to small price movements.

Key Factors Influencing Gamma

Moneyness (Price Position)

Gamma reaches its maximum peak when the option is At-the-Money (ATM). Conversely, it drops to its lowest levels when the option moves deep In-the-Money (ITM) or deep Out-of-the-Money (OTM).

Time to Expiration

For ATM options, Gamma increases significantly as the expiration date approaches. This acceleration creates higher price sensitivity in the final days of the contract.

Implied Volatility (IV)

Gamma moves inversely to volatility. As IV rises, Gamma decreases because the higher volatility “spreads out” the probability of price movement, flattening the delta curve.

Professional Summary

”In summary, Gamma acts as the ‘accelerator’ of an option’s price. It is most explosive for short-term, at-the-money contracts and tends to stabilize as volatility increases or as the option moves further away from the current market price.”

In conclusion, while Delta gives you a snapshot of your current exposure, Gamma provides the roadmap for how that exposure will evolve. Mastering Gamma is the difference between simply trading and truly managing a professional-grade portfolio.